Canada Gazette, Part I, Volume 147, Number 20: Regulations Amending the Renewable Fuels Regulations, 2013

May 18, 2013

Statutory authority

Canadian Environmental Protection Act, 1999

Sponsoring department

Department of the Environment

REGULATORY IMPACT ANALYSIS STATEMENT

(This statement is not part of the Regulations.)

1. Executive summary

Issue: The requirement of 2% renewable content in heating distillate oil under the Renewable Fuels Regulations could impact Canadian families that heat their homes using heating distillate oil, since the renewable content is relatively more expensive. Furthermore, the temporary exemption for Nova Scotia, New Brunswick, and Prince Edward Island from the 2% renewable content requirement in diesel fuel and heating distillate oil required primary suppliers for these Maritime provinces to have complied with the current regulatory requirements by January 1, 2013 — a date that some suppliers expressed difficulty in meeting.

Description: The proposed Regulations Amending the Renewable Fuels Regulations, 2013 (the proposed Amendments) would include a permanent nationwide exemption from the 2% renewable content requirement for heating distillate oil for space heating purposes (mostly home heating), as well as a six-month extension to the exemption for Nova Scotia, New Brunswick, and Prince Edward Island from the 2% renewable content requirement in both diesel fuel and heating distillate oil, ending June 30, 2013.

Cost-benefit statement: Fuel suppliers are expected to respond to the proposed Amendments by replacing some renewable fuel content with less costly diesel fuel. This would result in savings (avoided fuel costs) for industry and consumers, and some social costs due to foregone reductions in greenhouse gas (GHG) emissions. For the period 2013–2035, the present value of total benefits are estimated at $286 million from direct fuel cost savings for industry ($248 million) and consumers ($38 million). The present value of total costs are estimated at $51 million, based on 1.9 megatonnes (Mt) in total foregone GHG emissions reductions (averaging less than 0.1 Mt annually). The present value of net benefits is estimated to be almost $236 million, with total benefits outweighing total costs by a ratio of almost six to one.

“One-for-One” Rule and small business lens: Environment Canada has reviewed the administrative burden estimated to result from the proposed Amendments and has concluded that the “One-for-One” Rule does not apply, as there is no expected net change in administrative costs to businesses.

Similarly, Environment Canada has reviewed the impact of the proposed Amendments on small businesses and concluded that the small business lens does not apply, as no costs to small businesses are expected.

2. Background

The Renewable Fuels Regulations published in the Canada Gazette, Part Ⅱ, on September 1, 2010, (see footnote 1) included provisions requiring an average 2% renewable content in diesel fuel and heating distillate oil. The Regulations Amending the Renewable Fuels Regulations published in the Canada Gazette, Part Ⅱ, on July 20, 2011, (see footnote 2) specified the coming into force date of July 1, 2011 for the 2% renewable content requirement in diesel fuel and heating distillate oil, including a permanent exemption from the requirements for Newfoundland and Labrador, the Northwest Territories, Yukon, Nunavut and that part of Quebec that is north of latitude 60°N.

The 2011 regulatory Amendments also included a temporary exemption from the requirements for Nova Scotia, New Brunswick, Prince Edward Island (the Maritime provinces) and that part of Quebec that is on or south of latitude 60°N on or before December 31, 2012.

The intent to propose new regulatory Amendments was announced by Environment Minister Peter Kent on December 31, 2012. The announcement outlined the following: a permanent national exemption for the 2% renewable content requirement for home heating oil, as well as a six-month extension to the exemption for the Maritime provinces from the 2% renewable content requirement in both diesel fuel and heating distillate oil.

3. Issue

The requirement of 2% renewable content in heating distillate oil under the Renewable Fuels Regulations could impact Canadian families that heat their homes using heating distillate oil, since the renewable content is relatively more expensive.

Furthermore, the existing expiration date for the exemption for the Maritime provinces from the 2% renewable content requirement in both diesel fuel and heating distillate oil in the current Regulations required suppliers of distillates to the Maritime provinces to have complied with the full regulatory requirements by January 1, 2013 — a date that some suppliers expressed difficulty in meeting.

4. Objectives

As announced by Minister Kent, the exemption from the regulatory requirement of the 2% renewable content for heating distillate oil is intended to mitigate cost increases for Canadians that use oil to heat their homes. The six-month extension to the exemption for the Maritime provinces from the 2% renewable content requirement in both diesel fuel and heating distillate oil would give regulatees supplying distillates to the Maritime provinces extra time to comply with the regulatory requirements.

5. Description

The proposed Amendments include amending section 6 of the Regulations to allow primary suppliers to subtract from their distillate pool diesel fuel or heating distillate oil sold for or delivered for use for space heating purposes (which covers over 80% of total heating distillate oil, including all home heating oil). (see footnote 3)

Section 6 would also be amended to allow primary suppliers to subtract from their distillate pool all diesel fuel or heating distillate oil sold for or delivered for use in the Maritime provinces during the period from January 1, 2013, to June 30, 2013.

In order to allow suppliers more time to adjust to these proposed changes in compliance requirements, the proposed Amendments include an extension to the compliance period beginning on January 1, 2013, increasing it from one to two years, to end on December 31, 2014.

Also included in the proposed Amendments is an interim report covering the period from January 1, 2013, to December 31, 2013, for distillate volumes and distillate compliance units, a 15-day extension to certain record-keeping and reporting requirements, an update to a reference standard and some other minor administrative amendments.

6. Regulatory and non-regulatory options considered

Status quo

The exemption for diesel fuel or heating distillate oil sold for or delivered for use in the Maritime provinces ended on December 31, 2012. The status quo would not provide primary suppliers of distillates to the Maritime provinces more time and flexibility to meet the required distillate blending requirements. In addition, the current Regulations do not have provisions to allow primary suppliers to subtract volumes of diesel fuel or heating distillate oil sold for or delivered for use for space heating purposes from their distillate pool, as targeted by the proposal.

Amendments

There is no mechanism under the Canadian Environmental Protection Act, 1999 (CEPA 1999) to implement, through non-regulatory means, the proposed changes to these Regulations. Therefore, the proposed Amendments are the only option available to achieve the stated policy objectives.

7. Benefits and costs

An analysis of the benefits and costs of the proposed Amendments was conducted to estimate the incremental impacts of the proposed Regulations on key stakeholders, including the Canadian public, industry and government. Under this analysis, fuel suppliers are expected to respond to the proposed Amendments by replacing some renewable fuel with less costly diesel fuel. This would result in some savings (avoided fuel costs) for both industry and consumers, but also some social costs due to foregone reductions in greenhouse gas (GHG) emissions.

For the period 2013–2035, the incremental impacts of the proposed Amendments have been quantified, monetized and discounted to present value (in 2013). The present value of total benefits is estimated at $286 million from direct fuel cost savings for industry ($248 million) and consumers ($38 million). The present value of total costs is estimated at $51 million, based on 1.9 megatonnes (Mt) in total foregone GHG emissions reductions (averaging less than 0.1 Mt annually). The present value of net benefits is estimated to be almost $236 million over 23 years, with benefits outweighing costs by a ratio of almost six to one.

7.1. Overall cost-benefit analysis (CBA) approach

This analysis of benefits and costs follows the Treasury Board Secretariat CBA guidelines (www.tbs-sct.gc.ca/rtrap-parfa/analys/analystb-eng.asp), including the following key elements:

- Current analysis: The analysis adopts a 2013 perspective in terms of using best available information about the response behaviour of key stakeholders to the current Regulations, and projected future economic trends.

- Incremental impacts: The proposed Amendments are evaluated as a “regulatory” scenario in terms of their relative impacts compared to a baseline “business as usual” (BAU) scenario.

- Time frame for analysis: The time horizon used for evaluating the incremental impacts of the proposed Amendments is 23 years and covers the period from January 1, 2013, to December 31, 2035, based on available modelling tools and consistent with other regulatory analyses.

- Quantification and monetization: The analysis attempts to identify all significant incremental impacts as costs or benefits, estimate them in quantitative terms, and monetize them in 2012 Canadian dollars. Whenever quantification or monetization was not possible, impacts have been presented qualitatively.

- Discount rate: The Treasury Board Secretariat's 3% social discount rate was used to calculate the present value of costs and benefits, consistent with other GHG regulatory analyses.

7.2. Current analysis and key assumptions

Recent information has indicated that compliance behaviour has been and is expected to be different than previously expected in the Regulatory Impact Analysis Statement (RIAS) for the Regulations Amending the Renewable Fuels Regulations published in the Canada Gazette, Part Ⅱ, on July 20, 2011. As a result, the estimates from this cost-benefit analysis are not directly comparable to the original analysis of the 2% renewable content requirement in diesel fuel and heating distillate oil.

Renewable content blending by primary suppliers has been reported for the initial compliance period of the 2% renewable content requirement in diesel fuel and heating distillate oil. As well, suppliers of diesel fuel and heating distillate oil to Quebec and the Maritimes, where volumes have been exempted until December 31, 2012, have stated a preference toward blending hydrogenation-derived renewable diesel (HDRD) into diesel fuel to meet their obligations under the Renewable Fuels Regulations. This information, as well as consultation with industry and government experts, has informed the understanding of the world today as it pertains to meeting the blending requirements under the Regulations.

Moving forward, it is expected that renewable fuel content will consist of roughly 90% imports and 10% domestic product to meet federal regulatory requirements. Also, primary suppliers have demonstrated a preference to almost exclusively create blends with diesel fuel to meet their renewable content obligations for both diesel fuel and heating distillate oil. As well, primary suppliers have chosen to blend HDRD year-round and canola-based biodiesel during the warmer months. This almost completely reduces the need for kerosene blending to improve the cold-flow properties of blended fuel. (see footnote 4), (see footnote 5) HDRD is expected to represent over 95% of renewable content blending in Eastern Canada, where the majority of national heating distillate oil volumes are sold (97% in 2011). (see footnote 6) These HDRD imports are expected to be roughly 70% palm-based and 30% tallow-based.

Expected trends related to regulatory compliance behaviour and consultation with industry and government experts have informed the following assumptions used for the period 2013–2035 of this cost-benefit analysis:

| Key variable | Assumption |

|---|---|

| Renewable content blending | All renewable content blended with diesel fuel |

| Renewable content reductions | Met entirely by reduced HDRD imports |

| HDRD composition (feedstocks) | 70% palm, 30% tallow |

| HDRD price | 40¢/L over diesel in 2013, falling to 30¢/L by 2018 |

| Incremental kerosene volumes | No expected incremental impact |

| Incremental capital, operating, maintenance, and administrative costs | No expected incremental impact |

7.3. Analytical scenarios

The analysis considers two analytical scenarios: a business as usual scenario (BAU) where the proposed Amendments are not implemented, and a regulatory scenario where the proposed Amendments are implemented. The difference between the two scenarios provides an estimate of the incremental impacts of the proposed Amendments. The two scenarios are based on the same energy demand and price forecasts for 2013–2035 and are limited in scope to the specific volumes of distillate relevant to the proposed Amendments. Both scenarios reflect the best understanding of the world today, recent information and expected trends regarding the compliance behaviour of fuel suppliers in response to their renewable content obligations under the Renewable Fuels Regulations.

7.3.1. Business as usual scenario

The business as usual scenario is defined by the absence of the proposed Amendments. In this baseline scenario, it is estimated that refiners would be required to blend an additional 48.5 megalitres (ML) of renewable content in 2013 and 41.2 ML in 2035 to meet the renewable content requirements in the absence of the space heating exemption, and 20.8 ML of renewable content in 2013 to meet the renewable content requirements in the absence of the Maritimes exemption extension. Recent trends (see section 7.2) would suggest the renewable content blended would likely have been almost exclusively HDRD in the short term, and this assumption is held throughout the analytical time frame. The lower energy content per litre of HDRD relative to petroleum diesel would have entailed additional fuel purchases by consumers to satisfy their total energy demand. (see footnote 7)

7.3.2. Regulatory scenario

The regulatory scenario is defined by the implementation of the proposed Amendments; petroleum diesel would replace the renewable content that would have otherwise been required. Less fuel would be required to meet the total energy demand since diesel has a higher energy content per litre than does HDRD, meaning fuel savings for consumers. Since petroleum diesel has higher GHG emissions than do renewable alternatives, GHG emissions are estimated to be higher in the regulatory scenario.

7.4. Modelling and data

Heating distillate oil and diesel demand forecasts were required to estimate the expected reduction of renewable content as a result of these proposed Amendments. Fuel characteristics such as energy content, GHG emissions factors, and prices were also required to complete the cost-benefit analysis. A social cost of carbon was used to estimate socioeconomic damages due to GHG emissions.

7.4.1. Heating distillate oil demand forecast

Environment Canada's Energy-Economy-Environment Model for Canada (E3MC) was used to forecast volumes of heating distillate oil for 2013–2035 and volumes of diesel fuel for 2013. The E3MC is an end-use model that incorporates historical data from the National Inventory Report published by Environment Canada's Pollution Inventories and Reporting Division (PIRD).

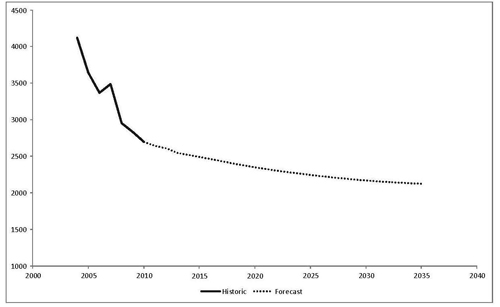

The volume of diesel fuel used for space heating purposes is negligible, so only a forecast of heating distillate oil for space heating purposes was necessary for the analysis of the national space heating exemption. Figure 1 shows the demand for heating distillate oil for space heating purposes nationally, excluding Newfoundland and Labrador and the Territories, historical data to 2010, and the forecast for 2011–2035, as described above.

Figure 1: Demand for heating distillate oil for space heating purposes (ML) (see footnote 8)

Source: E3MC; ML = megalitres

7.4.2. Relevant distillate volumes

Only certain volumes of diesel fuel and heating distillate oil are relevant to the analysis of the proposed Amendments.

For the national space heating exemption, relevant volumes of heating distillate oil are those used for space heating purposes over 2013–2035 for Alberta, Saskatchewan, Manitoba, Ontario, Quebec, New Brunswick, Nova Scotia, and Prince Edward Island. (see footnote 9)

For the Maritimes exemption extension, relevant volumes of diesel fuel are those sold for or delivered for use in the Maritime provinces during the first half of 2013. This was estimated by multiplying the forecasted demand by the historical proportion of diesel fuel sold in these provinces between January 1 and June 30, 2011. (see footnote 10) As well, volumes of heating distillate oil not used for space heating purposes in these provinces in 2013 were accounted for by dividing their forecast annual volume in half. (see footnote 11)

7.4.3. Renewable content volumes

The Renewable Fuels Regulations require 2% renewable content based on the pre-blended volumes of diesel fuel and heating distillate oil subject to the Regulations. The final blended product would therefore average 1.96% renewable content. (see footnote 12) To determine the reduction in renewable content volumes, the relevant volumes of distillates were multiplied by 1.96%. (see footnote 13)

For the space heating exemption, compliance units would be created for volumes of distillates used for space heating in British Columbia, since the provincial regulations would continue to require 4% renewable content. (see footnote 14) This would be expected to reduce actual renewable content volumes under the Renewable Fuels Regulations by an amount equal to the compliance units created.

7.4.4. Fuel energy content

HDRD has roughly a 5.5% lower average volumetric energy density than petroleum diesel. (see footnote 15) Table 2 shows the average energy density of petroleum diesel and HDRD from palm and tallow feedstocks in megajoules per litre (MJ/L). The energy density of these fuels is used to determine the volume of fuel required to meet a certain energy demand.

| Fuel type | Energy density (MJ/L) |

|---|---|

| Petroleum diesel | 38.653 |

| HDRD (from palm) | 36.511 |

| HDRD (from tallow) | 36.511 |

7.4.5. Fuel GHG emissions factors

Life cycle emission factors for diesel fuel and HDRD (from palm and tallow) were estimated using Natural Resources Canada's (NRCan) GHGenius model, version 4.02a, under average Canadian conditions, in order to inform estimates of incremental GHG emissions due to the proposed Amendments. The GHG emission factors are presented in Table 3 below (e.g. in the case of diesel, 1 L of petroleum diesel used in an internal combustion engine results in approximately 3.506 kg of CO2e emissions on a life cycle basis, which accounts for all emissions from production and combustion). These emissions factors are used to determine the emissions from the fuel consumed in both the business as usual and regulatory scenarios.

| Fuel type | Emissions (kgCO2e/L) |

|---|---|

| Petroleum diesel | 3.506 |

| HDRD (from palm) | 1.877 |

| HDRD (from tallow) | 0.544 |

7.4.6. Fuel prices

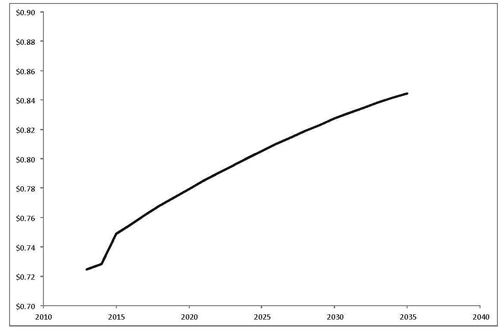

Pre-tax retail diesel price projections were forecast for 2013–2035 using E3MC. The E3MC incorporates the National Energy Board's (NEB) forecast for the West Texas Intermediate crude oil price as reported in the NEB's Canada's Energy Future: Energy Supply and Demand Projections to 2035 — Market Energy Assessment. (see footnote 18) The E3MC uses this data to generate fuel price forecasts which are primarily based on consumer-choice modelling and historical relationships between macroeconomic and fuel price variables. To estimate wholesale diesel prices, the pre-tax diesel prices were reduced by a 2012 national average marketing operating margin of 9.7¢/L retrieved from Kent Marketing Services. (see footnote 19) Figure 2 below shows the pre-tax wholesale diesel price forecast for 2013–2035.

Prices for HDRD were assumed to be approximately 40¢/L higher than diesel prices in 2013, based on best available information from industry experts and stakeholder consultations. It is expected that the HDRD supply will increase in the coming years as additional production comes online, and the price is thus expected to fall. Based on industry experts, the HDRD price premium over diesel is assumed to decrease from 40¢/L to 30¢/L over the next five years, which is roughly on par with the current price premium for biodiesel over diesel. The HDRD price is assumed to maintain a 30¢/L margin over diesel for the remainder of the forecast period.

Figure 2: Pre-tax, wholesale diesel price per litre in 2012 Canadian dollars

Source: E3MC

7.4.7. Social cost of carbon

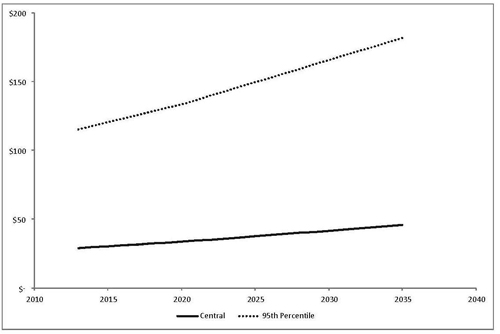

The estimated value of avoided damages from GHG reductions is based on the climate change damages avoided at the global level. These damages are usually referred to as the social cost of carbon (SCC). Estimates of the SCC between and within countries vary widely due to challenges in predicting future emissions, climate change, damages and determining the appropriate weight to place on future costs relative to near-term costs (discount rate) and foreign damages relative to domestic damages.

The SCC values used in this assessment draw on ongoing work undertaken by Environment Canada (see footnote 20) in collaboration with a federal interdepartmental working group, and in consultation with a number of external academic experts. This work involves reviewing existing literature and other countries' approaches to valuing GHG emissions. Preliminary recommendations, based on current literature and in line with the approach adopted by the U.S.

Interagency Working Group on the Social Cost of Carbon, (see footnote 21) are that it is reasonable to estimate SCC values at $29.06/tonne of CO2e in 2013, increasing each year with the expected growth in damages. (see footnote 22) Environment Canada's review also concludes that a value of $115.18/tonne in 2013 should be considered, reflecting arguments raised by Weitzman (2011) (see footnote 23) and Pindyck (2011) (see footnote 24) regarding the treatment of right-skewed probability distributions of the SCC in cost-benefit analyses. (see footnote 25) Their argument calls for full consideration of low probability, high-cost climate damage scenarios in cost-benefit analyses to more accurately reflect risk. A value of $115.18/tonne does not, however, reflect the extreme end of SCC estimates, as some studies have produced values exceeding $1,000/tonne of carbon emitted.

The federal interdepartmental working group on SCC also concluded that it is necessary to continually review the above estimates in order to incorporate advances in physical sciences, economic literature, and modelling to ensure the SCC estimates remain current. Environment Canada will continue to collaborate with the federal interdepartmental working group and outside experts to review and incorporate, as appropriate, new research on SCC in the future.

Figure 3: SCC estimates (2012 Canadian dollars per tonne)

Source: Federal interdepartmental working group on the social cost of carbon

7.5. Benefits

The proposed Amendments would result in supplier and consumer fuel savings due to the reduced renewable content requirements. Primary suppliers have demonstrated a preference to almost exclusively create blends with diesel fuel to meet their renewable content obligations for both diesel fuel and heating distillate oil. This means that any renewable content reductions would be replaced by less expensive diesel fuel, resulting in fuel cost savings for suppliers. Diesel also has a slightly higher energy content than does renewable fuel, meaning that consumers would need less fuel to meet their energy demands, resulting in direct fuel savings for consumers.

7.5.1. Supplier fuel cost savings

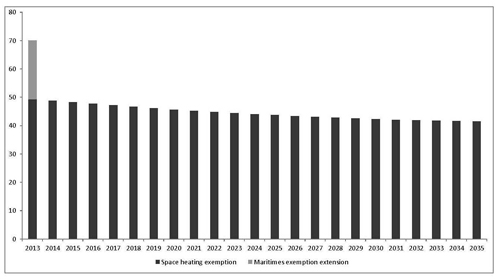

The proposed Amendments would reduce the renewable content obligations for primary suppliers of diesel fuel and heating distillate oil to the Maritimes in 2013, and for primary suppliers of heating distillate oil for space heating purposes nationally from 2013 onwards. Figure 4 shows the estimated incremental reduction in renewable content as a result of the proposed Amendments. (see footnote 26) The decreasing trend in incremental reductions in renewable content over the period 2013–2035 reflects the forecast decrease in relevant heating distillate oil demand, as shown previously in Figure 1. The incremental reductions from the Maritimes exemption extension are assumed to occur in 2013, although the extended compliance period for 2013–2014 may imply some reallocation across these two years.

Figure 4: Yearly incremental reductions in renewable content (ML) (see footnote 27)

Source: modelling results as described in sections 7.4.1 to 7.4.4; ML = megalitres

Large cost reductions would be realized due to reduced imports of HDRD. These would be partially offset by increased diesel purchases to replace the volume of renewable fuel reduced. (see footnote 28) The net result would be fuel cost savings to suppliers, as shown in table 4 below.

The present value of cost reductions from reduced HDRD imports as a result of the space heating exemption is estimated to be $832.3 million for 2013–2035. The cost of increased diesel purchases over this period is estimated to be $592.6 million, resulting in net supplier fuel cost savings of $239.7 million for the space heating exemption.

The Maritimes exemption extension is expected to result in cost reductions from reduced HDRD imports estimated at $23.4 million in 2013. The cost of increased diesel purchases is estimated to be $15.1 million in 2013, resulting in net supplier fuel cost savings of $8.3 million from the Maritimes exemption extension.

Overall, the proposed Amendments would be expected to result in supplier fuel cost savings, over the period 2013–2035, estimated at a present value of $248.0 million.

| Fuel savings (and offsetting costs) | 2013 | 2023 | 2035 | 2013–2035 (PV) |

|---|---|---|---|---|

| Space heating exemption | ||||

| HDRD import cost reductions | 54.5 | 48.0 | 47.2 | 832.3 |

| Cost of increased diesel purchases | (35.1) | (34.9) | (34.8) | (592.6) |

| Net fuel cost savings | 19.4 | 13.2 | 12.4 | 239.7 |

| Maritimes exemption extension | ||||

| HDRD import cost reductions | 23.4 | 0.0 | 0.0 | 23.4 |

| Cost of increased diesel purchases | (15.1) | (0.0) | (0.0) | (15.1) |

| Net fuel cost savings | 8.3 | 0.0 | 0.0 | 8.3 |

| Total net fuel cost savings | 27.7 | 13.2 | 12.4 | 248.0 |

Note: Due to rounding, some of the totals may not match; PV = present value discounted to 2013 at a 3% discount rate.

In this analysis, net supplier fuel cost savings represent avoided costs of the current Regulations, and some of this benefit may be passed onto consumers of diesel fuel or heating distillate oil.

7.5.2. Consumer fuel savings

A 1.96% final blend of HDRD in diesel constitutes a 0.11% reduction in energy content per litre compared to the average energy content of petroleum diesel. On an individual basis, this reduction in volumetric energy content would not result in a noticeable increase in fuel consumption. At the national level, however, much larger volumes of fuel are considered, and it is important to account for this small energy difference.

The proposed Amendments would see some renewable content replaced by petroleum diesel. The result would be some cost savings to Canadian end-users since less purchased diesel volume would be required in order to meet the same total energy demand. Reduced fuel purchases from the space heating exemption would be expected to be about 56.7 ML for 2013–2035, with an estimated present value of $37.3 million. (see footnote 29) The Maritimes exemption extension would be expected to result in reduced fuel purchases of about 1.2 ML in 2013, with cost savings estimated at a present value of $0.9 million. The total present value of reduced fuel purchases as a result of these proposed Amendments is estimated to be $38.3 million, as shown in Table 5 below.

| exemptions | 2013 | 2023 | 2035 | 2013–2035 (PV) |

|---|---|---|---|---|

| Space heating exemption | 2.2 | 2.2 | 2.2 | 37.3 |

| Maritimes exemption extension | 0.9 | 0 | 0 | 0.9 |

| Total incremental benefit | 3.2 | 2.2 | 2.2 | 38.3 |

Note: Due to rounding, some of the totals may not match; PV = present value discounted to 2013 at a 3% discount rate.

7.5.3. Total benefits

The present value of total benefits from the space heating exemption from the Renewable Fuels Regulations is estimated to be $277.0 million. The Maritimes exemption extension would result in a present value of total benefits estimated at $9.3 million. The total benefits from the proposed Amendments are thus estimated to be $286.3 million (present value), as shown in Table 6 below.

| exemptions | 2013 | 2023 | 2035 | 2013–2035 (PV) |

|---|---|---|---|---|

| Space heating exemption | 21.6 | 11.4 | 7.6 | 277.0 |

| Maritimes exemption extension | 9.3 | 0.0 | 0.0 | 9.3 |

| Total benefits | 30.9 | 11.4 | 7.6 | 286.3 |

Note: Due to rounding, some of the totals may not match; PV = present value discounted to 2013 at a 3% discount rate.

7.6. Costs

The proposed Amendments would result in foregone GHG emissions reductions due to the reduced renewable content requirements for primary suppliers. These GHG emissions are the only quantified cost in this analysis, and are monetized using a social cost of carbon of about $29 per tonne in 2013.

7.6.1. Foregone GHG emissions reductions

GHGenius life cycle assessment (LCA) modelling (see footnote 30) estimates that GHG emissions by volume are higher for petroleum diesel than for HDRD. The proposed Amendments would be expected to result in reduced HDRD content and increased petroleum content in diesel fuel, resulting in an increase in GHG emissions. This would be partially offset by an overall reduction in fuel purchases since the diesel pool would include less renewable content, which has a lower energy content. The net result would be an increase in GHG emissions due to these proposed Amendments.

As a result of the space heating exemption, it is estimated that the foregone GHG emissions reductions would be less than 0.1 Mt per year over the period 2013–2035. The Maritimes exemption extension would result in approximately 0.04 Mt in GHG emissions in 2013. For the period 2013–2035, the proposed Amendments would result in a total of 1.9 Mt of GHG emissions in the business as usual scenario, as shown in Table 7 below.

| exemptions | 2013 | 2023 | 2035 | 2013–2035 |

|---|---|---|---|---|

| Space heating exemption | 0.09 | 0.08 | 0.08 | 1.86 |

| Maritimes exemption extension | 0.04 | 0.00 | 0.00 | 0.04 |

| Total incremental emissions | 0.13 | 0.08 | 0.08 | 1.90 |

Note: Due to rounding, some of the totals may not match.

The incremental GHG emissions that would result from the proposed Amendments are monetized in Table 8 below, based on the central value for the social cost of carbon of $29.06 in 2013 (and increasing thereafter), as shown previously in Figure 3.

The present value of total costs from the space heating exemption from the Renewable Fuels Regulations is estimated to be $49.4 million. The present value of total costs from the Maritimes exemption is estimated at $1.1 million. The total costs from the proposed Amendments are thus estimated to be $50.5 million (present value) based on the central value for the social cost of carbon. The results are presented below in Table 8.

| exemptions | 2013 | 2023 | 2035 | 2013–2035 (PV) |

|---|---|---|---|---|

| Space heating exemption | 2.6 | 2.9 | 3.5 | 49.4 |

| Maritimes exemption extension | 1.1 | 0 | 0 | 1.1 |

| Total incremental cost | 3.7 | 2.9 | 3.5 | 50.5 |

Note: Due to rounding, some of the totals may not match; PV = present value discounted to 2013 at a 3% discount rate.

7.7. Summary of costs and benefits

For the period 2013–2035, the present value of total benefits is estimated at $286 million from direct fuel cost savings for industry ($248 million) and consumers ($38 million). The present value of total costs is estimated at $51 million, based on foregone GHG emissions reductions of 1.9 million tonnes (megatonnes) valued at a social cost of carbon of about $29 per tonne in 2013. The present value of net benefits is estimated to be almost $236 million over 23 years, with benefits outweighing costs by a ratio of almost six to one. The results of the cost-benefit analysis of the proposed Amendments are presented in Table 9.

| Incremental costs and benefits (million 2012 CAN$) | Base Year: 2013 | 2023 | Final Year: 2035 | Total 23 Year (PV) 2013–2035 |

|---|---|---|---|---|

| Quantified industry benefits | ||||

| Supplier fuel cost savings | 27.7 | 13.2 | 12.4 | 248.0 |

| Quantified consumer benefits | ||||

| Consumer fuel cost savings | 3.2 | 2.2 | 2.2 | 38.3 |

| Total benefits | 30.9 | 15.3 | 14.5 | 286.3 |

| Quantified social costs | ||||

| GHG emissions (SCC at $29/tonne) | 3.7 | 2.9 | 3.5 | 50.5 |

| Total costs | 3.7 | 2.9 | 3.5 | 50.5 |

| Net benefit (SCC at $29/tonne) | 27.2 | 12.4 | 11.1 | 235.7 |

| Net benefit (alternate SCC at $115/tonne) | 16.3 | 3.8 | 0.8 | 85.6 |

| Benefit-to-cost ratio (SCC at $29/tonne) | 8.4 | 5.3 | 4.2 | 5.7 |

| GHG emissions (Mt CO2e) | 0.1 | 0.1 | 0.1 | 1.9 |

Note: Due to rounding, some of the totals may not match; PV = present value discounted to 2013 at a 3% discount rate.

7.7.1. Sensitivity analysis

A sensitivity analysis was done to consider the impact of uncertainty in key variables (i.e. changes in diesel and heating oil demand, HDRD price premium, and discount rates). The sensitivity analysis shows that the results are robust in terms of demonstrating positive net benefits for the proposed Amendments across a broad range of plausible values for these variables.

| Sensitivity variables | Net Benefit (PV) | ||

|---|---|---|---|

| Lower | Central | Higher | |

| Sensitivity to diesel and heating oil demand (-30%, central, +30%) | 165.0 | 235.7 | 306.4 |

| Sensitivity to HDRD price premium (-30%, central, +30%) | 161.3 | 235.7 | 310.1 |

| Sensitivity to discount rates (7%, 3%, undiscounted) | 176.4 | 235.7 | 308.4 |

Note: PV = Present value discounted to 2013 at a 3% discount rate.

7.7.2. Quantified impacts

Foregone GHG emissions reductions: The proposed Amendments are expected to result in foregone GHG emissions reductions as a result of the increased GHG emissions from diesel relative to HDRD on a lifecycle basis. The foregone GHG emissions reductions are estimated at less than 0.1 Mt per year on average, and total 1.9 Mt over the period 2013–2035.

Reduction in HDRD imports: The proposed Amendments are expected to result in a reduction in HDRD imports in response to the reduced renewable content obligations that primary suppliers would be required to meet. HDRD imports are estimated to be reduced by 1034.3 ML over the period 2013–2035.

7.8. Non-quantified impacts

7.8.1. Air quality and health impacts

The impacts on Canadian air quality from changes in mobile sector emissions due to biodiesel use were examined by Health Canada in 2011 for the Regulations Amending the Renewable Fuels Regulations. Results of national on-road use in Canada suggested very minimal impacts on mean ambient concentrations of PM2.5, tropospheric ozone (O3), carbon monoxide (CO), nitrogen dioxide (NO2) and sulphur dioxide (SO2). The human health implications of these changes in air quality were assessed nationally and indicated that some minimal health benefits would be expected in 2006, and that these would be reduced by 2020. The report is available at: www.hc-sc.gc.ca/ewh-semt/pubs/air/ biodiesel-eng.php.

Any incremental health impacts due to the changes in on-road emissions associated with the proposed Amendments are expected to be minimal.

7.8.2. Potential domestic biodiesel production

The proposed Amendments would reduce the demand for renewable fuel over the long term; the demand for renewable fuel is expected to decrease by 41.2 ML in 2035 as a result of the proposed Amendments. This reduced domestic demand for renewable fuel may reduce the domestic market for some biodiesel producers. The cost-benefit analysis assumes that the reduced renewable content would constitute a reduction in HDRD imports to reflect the reality of expected compliance behaviour.

7.8.3. Contracted volumes

Stakeholders have indicated that some primary suppliers have engaged in HDRD purchase contracts of one to two years. To ensure primary suppliers are not penalized for their efforts to comply with the Renewable Fuels Regulations, the proposed Amendments extend the compliance period for 2013 to two years from one. This is to provide primary suppliers with sufficient additional flexibility to reallocate compliance units throughout the longer compliance period. It is therefore expected that HDRD purchase contracts should not affect the total reductions assumed by the cost benefit analysis.

7.8.4. Government costs

The government has incurred costs in order to set up and monitor the regulations requiring 5% renewable content in gasoline. The incremental costs to set up and monitor the 2% requirement in diesel fuel and heating distillate oil were deemed to be negligible. These proposed Amendments would modify the 2% requirement and the incremental costs to government are expected again to be negligible.

7.9. Distributional impacts

Competitiveness

The Canadian economy is highly integrated with the U.S. economy. The Renewable Fuels Regulations would continue to require 2% renewable content for volumes of diesel fuel as prescribed in the Regulations. The United States have implemented similar requirements for renewable fuel content in diesel. No international competitiveness impacts on the refining industry are anticipated.

The proposed Amendments are intended to alleviate the short-term impact on the competitiveness of blenders and regional refiners and fuel importers in regions that have not been subject to provincial regulations, particularly in the Maritime provinces. The national refiners can make investments strategically in large markets and/or to meet national requirements by capitalizing on investments made in provinces where regulations already exist. The proposed Amendments provide an extended exemption period of six months for suppliers of distillates to the Maritime provinces, and additional flexibility in order to allow further time for industry to meet the requirements.

Renewable fuels facilities

The proposed Amendments would be expected to reduce domestic demand for renewable content by 69.3 ML in 2013 and an average of 43.9 ML annually thereafter. Although this reduction in domestic demand for renewable content is expected to be realized by a reduction in HDRD imports, it may also reduce the domestic market for some biodiesel producers. Primary suppliers would not be expected to make any change in capital investment decisions as a result of the proposed Amendments.

Supplier fuel costs

Savings (avoided fuel costs) resulting from the reduced renewable content obligations of primary suppliers would constitute a benefit to industry. Some of these savings may be passed on to consumers of either diesel fuel or heating distillate oil.

Consumer fuel costs

Overall, the proposed Amendments would be expected to mitigate fuel cost increases for Canadians, including those who use oil to heat their homes.

Fuel supply in the Maritimes

The Maritimes region of Canada has an average household income below that of the Canadian average, and a much higher per capita use of heating distillate oil for domestic heating purposes than the Canadian average. The six-month extension of the exemption for the Maritime provinces from the 2% renewable content requirement in diesel fuel and heating distillate oil would help reduce short-term risks of fuel supply disruptions to this region. The proposed Amendments would thus be expected to benefit the Maritimes region.

8. “One-for-One” Rule

The “One-for-One” Rule does not apply to the proposed Amendments, as there is no expected net change in administrative costs to businesses. The proposed Amendments would slightly alter some reporting details, but are not expected to impact on the overall frequency or intensity of reporting on an ongoing basis. The result is most likely to be no perceptible net change in the administrative burden on businesses.

9. Small business lens

The small business lens does not apply to the proposed Amendments as net costs to small businesses are not expected. Primary suppliers are the only regulatees for which a blending requirement applies, as related to their pool volumes; therefore, they are the only parties measurably and directly affected by the proposed Amendments. Primary suppliers have tended to be large business producers or importers of petroleum fuels and this is not expected to change in the foreseeable future.

10. Consultation

Since 2006, Environment Canada organized a number of consultation and information sessions with various stakeholders on the proposed regulatory approach for requiring renewable fuel content based on gasoline, diesel fuel and heating distillate oil volumes. A complete description of the consultation process, as well as responses to comments, was provided in the Regulatory Impact Analysis Statement (RIAS) for the Renewable Fuels Regulations published in the Canada Gazette, Part Ⅱ, on September 1, 2010, as well as in the RIAS for the Regulations Amending the Renewable Fuels Regulations published in the Canada Gazette, Part Ⅱ, on July 20, 2011.

On December 31, 2012, the Government announced that it intended to propose amendments and Environment Canada subsequently organized stakeholder information sessions and consultations on the proposed Amendments, including the following:

- In January and February 2013, Environment Canada held five information sessions via webinar to communicate the Minister's announcement, clarify aspects of the proposed Amendments, answer questions and consider comments. At the information sessions, Environment Canada also outlined the next steps in the regulatory development process.

- Environment Canada held a number of meetings and was in communication with individual stakeholders through February 2013 to follow up on questions and comments, and to ensure understanding of the proposed Amendments.

Through these consultations, briefings and information sessions, stakeholder views were collected for consideration. A summary of the comments expressed on specific issues during these consultations along with Environment Canada's response is provided below.

Regulatory process and timing implications

The proposed Amendments would allow primary suppliers to deduct from their distillate pools fuel oil sold or delivered for use for space heating purposes beginning on January 1, 2013. The proposed Amendments would also allow primary suppliers to deduct from their distillate pools fuel sold or delivered for use in the Maritime provinces during the period from January 1, 2013, to June 30, 2013. Given that the proposed Amendments would be published after the dates for which the proposed exemptions would be effective, some members of the petroleum industry were concerned about a period of regulatory uncertainty between January 1, 2013, and the date that the proposed Amendments would come into force. There were concerns that contractual obligations with renewable fuel producers would put primary suppliers at a financial disadvantage.

- Environment Canada proposes extending the second distillate compliance period from 12 to 24 months, which acknowledges recommendations from the petroleum industry. The extended compliance period, which would end on December 31, 2014, maintains the volume requirements of the current proposal while providing greater compliance flexibility.

Regional implications

Some regional members of the petroleum industry, while supportive of the permanent national exemption from the 2% renewable content requirement for home heating oil, commented that the six-month exemption extension should also apply to Quebec.

- Environment Canada has maintained the exemption extension as per the announced proposal.

Renewable fuel demand

Renewable fuel producers disagree with the proposed permanent national exemption from the renewable fuel content requirement for home heating oil, maintaining that the decreased demand for distillate compliance units would result in decreased market demand for biofuel suitable for blending with distillate. Concern was also expressed regarding the potential for further extensions to the proposed six-month extension to the exemption from the renewable fuel content requirement for diesel fuel and heating distillate oil sold or delivered for use in the Maritime provinces.

- The intention of the proposed Amendments is to mitigate the cost increases for Canadians who use oil to heat their homes and to provide flexibility for suppliers operating in the Maritime provinces to make the adjustments required to comply with the Regulations. Although the proposed Amendments would reduce the overall demand for renewable fuel, the amended Regulations would continue to create demand for renewable content in diesel fuel.

Distillate used for space heating purposes

Members of the petroleum industry expressed concern about how to identify heating distillate oil volumes in order to take advantage of the exemption.

- Environment Canada reviewed the scope for which the national exemption would apply. The proposed permanent national exemption is to apply to diesel fuel or heating distillate oil used solely for space heating purposes and not for powering industrial processes.

Other administrative concerns

Certain members of the petroleum industry requested that the Regulations include more time for recording information and creating records to facilitate more accurate record keeping.

- Environment Canada took into consideration the concerns of industry and included an administrative change that would provide two additional weeks of lead time for the recording of information and the making of records under the proposed Amendments.

On February 19, 2013, Environment Canada offered to consult with the Canadian Environmental Protection Act National Advisory Committee (CEPA NAC) on the proposed Amendments. CEPA NAC had 60 days from that date to accept the offer to consult.

11. Regulatory cooperation

Canada's Renewable Fuels Regulations are not a commitment under the Joint Action Plan for the Canada-United States Regulatory Cooperation Council, but were designed to generally align with the approach of the U.S. Environmental Protection Agency (EPA) Renewable Fuels Standard (RFS1) while being tailored to Canadian conditions. The United States have since implemented RFS2, which introduced the differentiation between types of renewable fuels based on their life cycle GHG emissions. After giving due consideration to the issue and taking into account the complexities and controversies of GHG lifecycle analysis, Environment Canada did not include mandates or differential treatment of renewable fuels based on GHG emissions. Though Canada's Regulations are not strictly aligned with those of the United States, they do not discriminate between domestic and imported fuels. Environment Canada meets regularly with the U.S. EPA to share knowledge and experience related to implementation of the respective regulations of both nations.

Requirements for renewable content in diesel fuel have been implemented by other jurisdictions as well, including the European Union and Brazil. Details of these requirements, along with those implemented in the United States, have been summarized in the RIAS for the Renewable Fuels Regulations published in the Canada Gazette, Part Ⅱ, on September 1, 2010, as well as in the RIAS for the Regulations Amending the Renewable Fuels Regulations published in the Canada Gazette, Part Ⅱ, on July 20, 2011.

Some provinces have established their own minimum renewable content requirements for distillates. The proposed Amendments are not expected to have an impact on any provincial requirements.

| Province | Regulated level |

|---|---|

| British Columbia | 4% |

| Alberta | 2% |

| Saskatchewan | 2% |

| Manitoba | 2% |

The federal Regulations promote an integrated and nationally consistent approach to achieving significant reductions in GHG emissions.

12. Rationale

An analysis of the benefits and costs of the proposed Amendments was conducted to estimate the incremental impacts of the proposed Regulations on key stakeholders, including the Canadian public, industry and Government.

Under this analysis, fuel suppliers are expected to respond to the proposed Amendments by displacing some renewable fuel with less costly diesel fuel which will result in savings (avoided fuel costs) to industry and consumers, but also some social costs due to foregone reductions in greenhouse gas (GHG) emissions.

The total benefits are estimated at $286 million from direct fuel cost savings for industry ($248 million) and for consumers ($38 million). At least some of the industry fuel savings are expected to be passed onto consumers.

The total costs are estimated at $51 million, based on foregone GHG emissions reductions of 1.9 Mt valued at a social cost of carbon of about $29 per tonne in 2013. The increase in estimated GHG emissions resulting from the proposed Amendments averages less than 0.1 Mt annually.

The present value of net benefits is estimated to be almost $236 million over 23 years, with benefits outweighing costs by a ratio of almost six to one. The proposed Amendments would also provide suppliers of distillates to the Maritime provinces with more time and flexibility to meet their renewable fuel blending obligations, which may reduce some short-term risks of fuel supply disruptions.

The amending Regulations will be made under the Fuels Division of the Canadian Environmental Protection Act, 1999. In order to make the Regulations, the Governor in Council must be of the opinion that the Regulations could make a significant contribution to the prevention of, or reduction in, air pollution. The two existing federal regulatory requirements for renewable fuel content (in gasoline and diesel) have been estimated to reduce GHG emissions by approximately 2 Mt per year. The current RIAS estimates forgone greenhouse gas emissions reductions at less than one tenth of one megatonne carbon dioxide equivalent (CO2e) per year. Thus the amended Regulations would continue to deliver a significant reduction in air pollution.

13. Implementation, enforcement and service standards

The proposed Amendments are not expected to increase government costs or administrative burden on regulatees. In addition to maintaining the compliance promotion and enforcement activities described under the current Regulations, the proposed Amendments would require an updated explanation of the Regulations and how they affect annual reporting. No monitoring activity changes are expected as a result of the proposed Amendments, and there are no service standards associated with the proposed Amendments.

Details on the above activities are provided in the RIAS for the Renewable Fuels Regulations published in the Canada Gazette, Part Ⅱ, on September 1, 2010, as well as the RIAS for the Regulations Amending the Renewable Fuels Regulations published in the Canada Gazette, Part Ⅱ, on July 20, 2011.

14. Performance measurement and evaluation

A detailed performance measurement and evaluation plan (PMEP) was developed for the Renewable Fuels Regulations. A description of the original PMEP was provided in the RIAS for the Renewable Fuels Regulations published in the Canada Gazette, Part Ⅱ, on September 1, 2010, as well as the RIAS for the Regulations Amending the Renewable Fuels Regulations published in the Canada Gazette, Part Ⅱ, on July 20, 2011. The PMEP is to be updated to reflect the proposed Amendments following the Canada Gazette, Part Ⅱ, publication, once finalized. The revised PMEP would be made available upon request from Environment Canada at that time.

15. Contacts

Leif Stephanson

Chief

Fuels Section

Oil, Gas and Alternative Energy Division

Environment Canada

351 Saint-Joseph Boulevard, 9th Floor

Gatineau, Quebec

K1A 0H3

Telephone: 819-953-4673

Fax: 819-953-8903

Email: fuels-carburants@ec.gc.ca

Yves Bourassa

Director

Regulatory Analysis and Valuation Division

Environment Canada

10 Wellington Street, 25th Floor

Gatineau, Quebec

K1A 0H3

Telephone: 819-953-7651

Fax: 819-953-3241

Email: RAVD.DARV@ec.gc.ca

PROPOSED REGULATORY TEXT

Notice is given, pursuant to subsection 332(1) (see footnote a) of the Canadian Environmental Protection Act, 1999 (see footnote b), that the Governor in Council proposes to make the annexed Regulations Amending the Renewable Fuels Regulations, 2013.

Any person may, within 60 days after the date of publication of this notice, file with the Minister of the Environment comments with respect to the proposed Regulations or a notice of objection requesting that a board of review be established under section 333 of that Act and stating the reasons for the objection. All comments and notices must cite the Canada Gazette, Part Ⅰ, and the date of publication of this notice, and be sent by mail to Leif Stephanson, Chief, Fuels Section, Oil, Gas and Alternative Energy Division, Energy and Transportation Directorate, Department of the Environment, Gatineau, Quebec K1A 0H3, by fax to 819-953-8903 or by email to fuels-carburants@ec.gc.ca.

Ottawa, May 9, 2013

JURICA ČAPKUN

Assistant Clerk of the Privy Council

REGULATIONS AMENDING THE RENEWABLE FUELS REGULATIONS, 2013 AMENDMENTS

1. (1) The definition “distillate compliance period” in subsection 1(1) of the Renewable Fuels Regulations (see footnote 31) is replaced by the following:

“distillate compliance period”

« période de conformité visant le distillat »

“distillate compliance period” means

- (a) the period that begins on July 1, 2011 and that ends on December 31, 2012;

- (b) the period that begins on January 1, 2013 and that ends on December 31, 2014; and

- (c) after December 31, 2014, each calendar year.

(2) Paragraph (b) of the definition “finished gasoline” in subsection 1(1) of the Regulations is replaced by the following:

- (b) has an antiknock index of at least 86, as determined by the applicable test method listed in the National Standard of Canada standard CAN/CGSB-3.5-2011, Automotive Gasoline.

(3) The portion of paragraph (b) of the definition “gasoline” before subparagraph (i) in subsection 1(1) of the Regulations is replaced by the following:

- (b) suitable for use in a spark-ignition engine and has the following characteristics, as determined by the applicable test method listed in the National Standard of Canada standard CAN/CGSB-3.5-2011, Automotive Gasoline:

2. (1) The portion of subsection 6(4) of the Regulations before paragraph (a) is replaced by the following:

Excluded volumes

(4) Despite subsections (1) and (2), a primary supplier may, before carrying forward any compliance units under section 21 or 22, subtract from their gasoline pool or distillate pool, as the case may be, the volume of a batch, or of a portion of the batch, of fuel in their pool if they make, before the end of the trading period in respect of the compliance period, a record that establishes that the volume was a volume of one of the following types of fuel:

(2) Subsection 6(4) of the Regulations is amended by adding the following after paragraph (f):

- (f.1) diesel fuel or heating distillate oil, as the case may be, sold for or delivered for use solely for space heating purposes and not for powering industrial processes;

(3) Paragraph 6(4)(h) of the French version of the Regulations is replaced by following:

- h) jusqu'au 31 décembre 2012 inclusivement, carburant diesel ou mazout de chauffage vendu ou livré pour usage en Nouvelle-Écosse, au Nouveau-Brunswick, à l'Île-du-Prince-Édouard et dans la partie de la province de Québec située au soixantième degré de latitude nord ou au sud de celle-ci;

(4) Subsection 6(4) of the Regulations is amended by adding the following after paragraph (h):

- (h.1) during the period that begins on January 1, 2013 and that ends on June 30, 2013, diesel fuel or heating distillate oil, as the case may be, sold for or delivered for use in Nova Scotia, New Brunswick and Prince Edward Island;

3. The description of DtGDD in subsection 8(2) of the Regulations is replaced by the following:

DtGDD is the volume, expressed in litres, that is equal to

- (a) for distillate compliance periods other than the first and second ones, the value that they assigned for DtGDG in subsection (1) for the gasoline compliance period that is the same period as the distillate compliance period,

- (b) for the first distillate compliance period, the total of the values that they assigned for DtGDG in subsection (1) for gasoline compliance periods that overlapped with the first distillate compliance period, and

- (c) for the second distillate compliance period, the total of the values that they assigned for DtGDG in subsection (1) for gasoline compliance periods that overlapped with the second distillate compliance period.

4. Section 19 of the Regulations is amended by adding the following after subsection (3):

Subsection 6(4) read out

(4) For the purpose of the determination referred to in subsection (1) or (2), section 6 is to be read without reference to its subsection (4).

5. Section 30 of the Regulations is replaced by the following:

Annual report

30. For each compliance period during which a primary supplier produces or imports gasoline, diesel fuel or heating distillate oil, they must, on or before April 30 following the end of the compliance period, send a report to the Minister that contains the information set out in Schedule 4 for the compliance period.

6. Subsection 31(3) of the Regulations is replaced by the following:

When record made

(3) The record must be made within 30 days after the end of the month for which the information is required to be recorded.

7. Subsection 32(7) of the Regulations is replaced by the following:

Record — section 19

(7) Within 30 days after the end of each month during a compliance period, a primary supplier must make a record of the number calculated in accordance with subsection 19(1) or (2), as the case may be, for that month.

8. Section 33 of the Regulations is replaced by the following:

Annual report

33. For each compliance period in respect of which a compliance unit is created, carried forward, carried back, transferred in trade, received in trade or cancelled by a participant, the participant must, on or before April 30 following the end of the compliance period, send a report to the Minister that contains the information set out in Schedule 5 for the compliance period.

9. Section 37 of the Regulations is replaced by the following:

When records made

37. Except as otherwise provided in these Regulations, records must be made as soon as feasible but no later than 30 days after the information to be recorded becomes available.

10. Section 39 of the Regulations is replaced by the following:

December 15, 2010 to December 31, 2011

(1) A person who would, if the first gasoline compliance period were to finish on December 31, 2011, be required to send a report under section 30 or 33 or subsection 34(4) or 36(2) must send an interim report to the Minister for the period that begins on December 15, 2010 and that ends on December 31, 2011 in accordance with that section or subsection but as if that period were the first gasoline compliance period.

January 1, 2013 to December 31, 2013

(2) A person who would, if the second distillate compliance period were to finish on December 31, 2013, be required to send a report under section 30 or 33 must send an interim report to the Minister for the period that begins on January 1, 2013 and that ends on December 31, 2013 in accordance with that section but as if that distillate compliance period ended on December 31, 2013.

COMING INTO FORCE

11. These Regulations come into force on the day on which they are registered.

[20-1-o]

footnote *- Footnote 1

Available at http://canadagazette.gc.ca/rp-pr/p2/2010/2010-09-01/html/sor-dors189-eng.html. - Footnote 2

Available at http://canadagazette.gc.ca/rp-pr/p2/2011/2011-07-20/html/sor-dors143-eng.html. - Footnote 3

Environment Canada's Energy-Economy-Environment Model for Canada (E3MC). - Footnote 4

The cloud points of canola-derived biodiesel (–3(C) and HDRD (–5( to –34(C, depending on grade) are lower than cloud points for tallow or soy-derived biodiesel (+15( and +2(C, respectively). - Footnote 5

HVO Product Handbook, Neste Oil, www.nesteoil.com/binary.asp?GUID=7A041F14-022A-4295-B1E4-1102585F5E3F. - Footnote 6

Statistics Canada. Supply and disposition of refined petroleum products. http://www5.statcan.gc.ca/cansim/a26?lang=eng&retrLang=eng&id=1340004&

tabMode=dataTable&srchLan=-1&p1=-1&p2=35. - Footnote 7

Empirically, the change in fuel consumption resulting from introducing renewable diesel at low level fuel blends (<5%) is difficult to estimate, partly due to the small scale of energy content changes relative to the margin of error, and considering confounding factors affecting fuel consumption. While fuel consumption depends on many factors, the expectation is that the difference in volumetric energy density is relevant enough on a national level to merit consideration in this analysis. - Footnote 8

Volumes exclude Newfoundland and Labrador, and the Territories, as they are exempt from the Renewable Fuels Regulations. - Footnote 9

The proposed Amendments would not directly reduce renewable content requirements for volumes of heating distillate oil for space heating in British Columbia since they would still be covered by existing provincial regulations. British Columbia's Renewable & Low Carbon Fuel Requirements Regulation is the only provincial renewable fuels regulation that requires renewable content in heating distillate oil. For more information, visit www.bclaws.ca/EPLibraries/bclaws_new/document/ID/freeside/00_08016_01#section2. - Footnote 10

Historical data on monthly diesel sales for these provinces in 2011 was obtained from Statistics Canada, Supply and disposition of refined petroleum products (http://www5.statcan.gc.ca/cansim/a26?lang=eng&retrLang=eng&id=1340004&

tabMode=dataTable&srchLan=-1&p1=-1&p2=35). - Footnote 11

These volumes represent heating distillate used in industrial processing. Half was used as the half-year factor in the absence of monthly data on these specific volumes, for which little seasonal variation would be expected. - Footnote 12

For example, 100 ML of petroleum distillate would require the addition of 2 ML (2%) of renewable content. The resulting 102 ML would contain 1.96% renewable content (2 Ă· 102). - Footnote 13

An adjustment was made to account for the renewable content in the additional fuel purchases required in the BAU. - Footnote 14

1.96% of these volumes would equal the amount of compliance units created. - Footnote 15

HVO Product Handbook, Neste Oil, www.nesteoil.com/binary.asp?GUID=7A041F14-022A-4295-B1E4-1102585F5E3F. - Footnote 16

Delucchi, Mark A. (2003) A Lifecycle Emissions Model (LEM): Lifecycle Emissions from Transportation Fuels, Motor Vehicles, Transportation Modes, Electricity Use, Heating and Cooking Fuels, and Materials; MAIN REPORT. Institute of Transportation Studies, University of California, Davis, Research Report UCD-ITS-RR-03-17-MAIN. - Footnote 17

GHGenius, version 4.02a. - Footnote 18

www.neb.gc.ca/clf-nsi/rnrgynfmtn/nrgyrprt/nrgyftr/2011/nrgsppldmndprjctn2035-eng.html#s2_1 - Footnote 19

www.kentmarketingservices.com - Footnote 20

Contact Environment Canada's Economic Analysis Directorate for any questions regarding methodology, rationale, or policy. - Footnote 21

Technical support document, U.S. Interagency Working Group on Social Cost of Carbon, IWGSCC, 2010, “Social Cost of Carbon for Regulatory Impact Analysis Under Executive Order 12866,” U.S. Government. - Footnote 22

The value of $29.06/tonne of CO2 in 2013 (in 2012 Canadian dollars) and its growth rate have been estimated using an arithmetic average of the three models PAGE, FUND, and DICE. - Footnote 23

“Fat-Tailed Uncertainty in the Economics of Catastrophic Climate Change,” Review of Environmental Economics and Policy, 5(2), pp. 275–292 (summer 2011). - Footnote 24

“Fat Tails, Thin Tails, and Climate Change Policy,” Review of Environmental Economics and Policy, summer 2011. - Footnote 25

The value of $115.18/tonne of CO2 in 2013 (in 2012 Canadian dollars) and its growth rate have been estimated using an arithmetic average of the two models PAGE and DICE. The FUND model has been excluded in this estimate because it does not include low probability, high-cost climate damage. - Footnote 26

This includes the renewable content in the additional fuel purchases required in the business as usual scenario, which are accounted for in consumer fuel savings. - Footnote 27

Yearly incremental reductions in renewable content were calculated using information in sections 7.4.1 to 7.4.4. - Footnote 28

The pre-tax, wholesale diesel price was used to estimate the cost of diesel purchases. - Footnote 29

The pre-tax, retail diesel price was used to estimate consumer fuel savings. - Footnote 30

For more information, visit www.ghgenius.ca/about.php. - Footnote 31

SOR/2010-189 - Footnote a

S.C. 2004, c. 15, s. 31 - Footnote b

S.C. 1999, c. 33